Starting a business in Canada is exciting, but one of the first decisions you’ll need to make is choosing the right legal structure. Many entrepreneurs struggle with the choice between an incorporated business and an unincorporated business.

The structure you choose can affect everything from taxes and liability protection to financing opportunities and long-term growth. Understanding the differences can help you make an informed decision and avoid costly mistakes down the road.

In this guide, we’ll compare incorporated and unincorporated businesses in Canada, explore the advantages and disadvantages of each, and explain which option may be best for your situation.

What Is an Unincorporated Business?

An unincorporated business is a business that is not legally separate from its owner or owners. The individual operating the business is personally responsible for its debts, obligations, and liabilities.

This is the simplest and most common way to start a business in Canada because it requires less paperwork and lower startup costs.

Types of Unincorporated Businesses in Canada

There are two primary types of unincorporated business structures:

Sole Proprietorship

A sole proprietorship is owned and operated by one person. The owner receives all profits but is also personally responsible for all debts and liabilities.

Common examples include:

- Freelancers

- Consultants

- Online store owners

- Tradespeople

- Independent contractors

General Partnership

A general partnership involves two or more individuals who operate a business together.

Each partner:

- Shares profits and losses

- Participates in management

- Has personal liability for business obligations

Partnership agreements are highly recommended to clearly define each partner’s responsibilities.

Advantages of an Unincorporated Business

Easy and Affordable Setup

Registering a sole proprietorship or partnership is generally faster and less expensive than incorporating.

Less Administrative Work

There are fewer compliance requirements compared to corporations.

Simplified Tax Reporting

Business income is typically reported directly on the owner’s personal income tax return.

Full Control

Sole proprietors maintain complete decision-making authority over their business.

Disadvantages of an Unincorporated Business

Unlimited Personal Liability

Perhaps the biggest drawback is that business liabilities become personal liabilities.

If the business faces legal action or debt obligations, personal assets such as:

- Homes

- Vehicles

- Savings accounts

may potentially be at risk.

Limited Access to Financing

Banks and investors often view unincorporated businesses as riskier than corporations.

Limited Growth Potential

As a business grows, the lack of liability protection and tax planning opportunities may become significant disadvantages.

What Is an Incorporated Business?

An incorporated business is a legal entity that exists separately from its owners.

When entrepreneurs decide to incorporate a business in Canada, they create a corporation that can:

- Own property

- Enter contracts

- Borrow money

- Sue and be sued

independently of its shareholders.

This legal separation is one of the primary reasons why many growing businesses choose incorporation.

Types of Incorporated Businesses in Canada

Several types of corporations exist in Canada.

Private Corporation

The most common structure for small and medium-sized businesses.

Characteristics include:

- Privately owned shares

- Limited number of shareholders

- Not publicly traded

Canadian-Controlled Private Corporation (CCPC)

A CCPC is a private corporation controlled by Canadian residents.

Benefits often include:

- Small business tax deductions

- Tax deferral opportunities

- Enhanced tax planning strategies

Professional Corporation

Certain regulated professionals may operate through professional corporations.

Examples include:

- Lawyers

- Dentists

- Physicians

- Accountants

Rules vary by province and profession.

Provincial Corporation

Businesses incorporated under provincial legislation operate primarily within a specific province.

An example would be an Ontario corporation, which is incorporated under Ontario’s Business Corporations Act.

Federal Corporation

Federal corporations are incorporated under the Canada Business Corporations Act and receive name protection across Canada.

Advantages of an Incorporated Business

Limited Liability Protection

One of the most significant benefits of incorporation is limited liability.

In most situations:

- Shareholders are not personally responsible for corporate debts.

- Personal assets receive additional protection.

- Legal risks are generally contained within the corporation.

Tax Planning Opportunities

Corporations may benefit from lower small business tax rates compared to personal income tax rates.

Additional strategies may include:

- Income splitting opportunities (where permitted)

- Retaining earnings inside the corporation

- Dividend planning

Enhanced Credibility

Many customers, suppliers, lenders, and investors perceive incorporated businesses as more established and professional.

Easier Access to Investment

Corporations can issue shares and attract investors more easily than unincorporated businesses.

Perpetual Existence

Unlike sole proprietorships, corporations can continue operating even if ownership changes.

Disadvantages of an Incorporated Business

Higher Startup Costs

Incorporation generally costs more than registering a sole proprietorship.

Additional Record Keeping

Corporations must maintain:

- Corporate minute books

- Annual filings

- Shareholder records

- Corporate resolutions

Separate Tax Returns

Corporations must file their own corporate income tax returns in addition to personal tax filings.

Increased Compliance Requirements

Directors and officers must meet various legal obligations under corporate legislation.

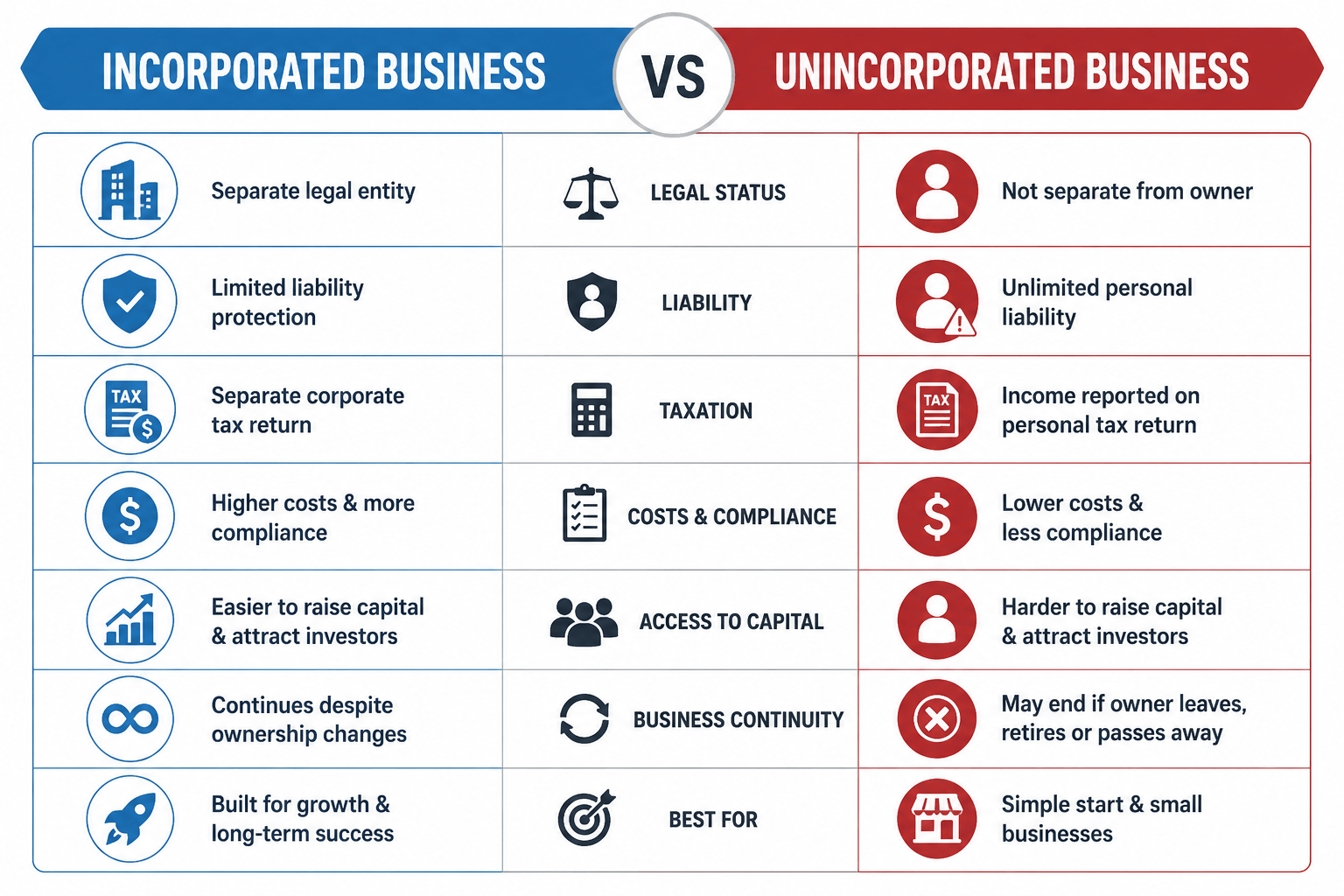

Incorporated Business vs Unincorporated Business: Side-by-Side Comparison

| Feature | Incorporated Business | Unincorporated Business |

|---|---|---|

| Legal Status | Separate legal entity from its owners | Owner and business are legally the same entity |

| Ownership | Owned by shareholders | Owned by one individual or partners |

| Liability Protection | Shareholders generally have limited liability | Owners have unlimited personal liability |

| Personal Assets Protection | Personal assets are generally protected from business debts and lawsuits | Personal assets may be at risk if the business incurs debts or legal claims |

| Business Debts | Corporation responsible for its own debts | Owner(s) are personally responsible for business debts |

| Tax Filing | Separate corporate tax return required | Business income reported on owner's personal tax return |

| Tax Planning Opportunities | Greater flexibility through salary, dividends, and retained earnings | Limited tax planning options |

| Startup Costs | Higher incorporation and setup costs | Lower registration costs |

| Annual Compliance | Corporate filings, annual returns, minute book maintenance | Minimal ongoing compliance requirements |

| Record Keeping | Extensive corporate records required | Simpler record keeping |

| Business Name Protection | Corporate name protected within jurisdiction of incorporation | Limited name protection |

| Access to Financing | Easier to obtain financing and attract investors | May face more challenges securing financing |

| Ability to Raise Capital | Can issue shares to investors | Cannot issue shares |

| Business Credibility | Often viewed as more professional and established | May be perceived as smaller or less formal |

| Business Continuity | Continues regardless of ownership changes | May cease if owner retires, dies, or leaves |

| Transfer of Ownership | Ownership transferred through sale of shares | More difficult to transfer ownership |

| Growth Potential | Well-suited for expansion and investment | Often better suited for small businesses and startups |

| Decision Making | Directors and shareholders may be involved | Owner has complete control (sole proprietorship) |

| Privacy | Some corporate information becomes publicly available | Generally fewer public disclosure requirements |

| Examples | Ontario Corporation, Federal Corporation, Professional Corporation, CCPC | Sole Proprietorship, General Partnership |

When Should You Choose an Unincorporated Business?

An unincorporated structure may be suitable if:

- You are testing a new business idea.

- Your business has minimal liability exposure.

- You want the lowest startup costs.

- Your annual revenue is relatively modest.

- You prefer simple tax reporting.

Many entrepreneurs begin as sole proprietors and incorporate later as the business grows.

When Should You Choose an Incorporated Business?

Incorporation may be a smart choice if:

- You want liability protection.

- You expect significant revenue growth.

- You plan to hire employees.

- You want to attract investors.

- You need greater business credibility.

- You wish to access corporate tax planning opportunities.

For many established businesses, incorporation becomes a strategic step toward long-term success.

Is an Ontario Corporation a Good Choice?

For entrepreneurs operating primarily in Ontario, forming an Ontario corporation can be an efficient and cost-effective option.

Benefits may include:

- Provincial incorporation fees

- Simplified provincial compliance

- Suitable structure for local operations

However, businesses planning to operate nationally may also consider federal incorporation.

The right choice depends on your growth plans, operating locations, and long-term objectives.

Frequently Asked Questions

Can I Change From a Sole Proprietorship to a Corporation Later?

Yes. Many business owners start as sole proprietors and incorporate once their revenue, risk exposure, or growth opportunities increase.

Does Incorporation Eliminate All Personal Liability?

No, Directors and officers can still have personal responsibilities under certain laws and regulations. Professional advice should be obtained for specific situations.

Is Incorporation Required to Operate a Business in Canada?

No, Many successful businesses operate as sole proprietorships or partnerships.

Which Structure Pays Less Tax?

The answer depends on your income level, business activities, and financial goals. Corporate tax planning can offer advantages, but professional tax advice is recommended.

Conclusion

Choosing between an incorporated business and an unincorporated business is one of the most important decisions a Canadian entrepreneur will make.

An unincorporated business offers simplicity, lower startup costs, and easier administration, making it ideal for many new entrepreneurs.

An incorporated business provides liability protection, tax planning opportunities, increased credibility, and stronger growth potential.

There is no one-size-fits-all answer. The best structure depends on your business goals, risk tolerance, industry, and future plans. Understanding the key differences between these structures will help you build a solid foundation for long-term success in Canada.